2026 Global Jewellery Sourcing Barometer: High-Growth Markets & Top Materials Revealed

To gauge sentiment towards the global jewellery market, a HKTDC survey was conducted among 1,507 of the jewellery buyers and exhibitors attending the leading industry events, namely the Hong Kong International Jewellery Show and the Hong Kong International Diamond, Gem & Pearl Show, in early March this year in Hong Kong.

Overall, many jewellery traders were somewhat cautious as to their 2026 prospects. It was acknowledged that the resilience of the jewellery industry was largely down to its facility for strategic diversification.

This article will present detailed survey findings for jewellery industry players’ better strategic positioning.

How Confident Are Jewellery Traders On the Market Outlook?

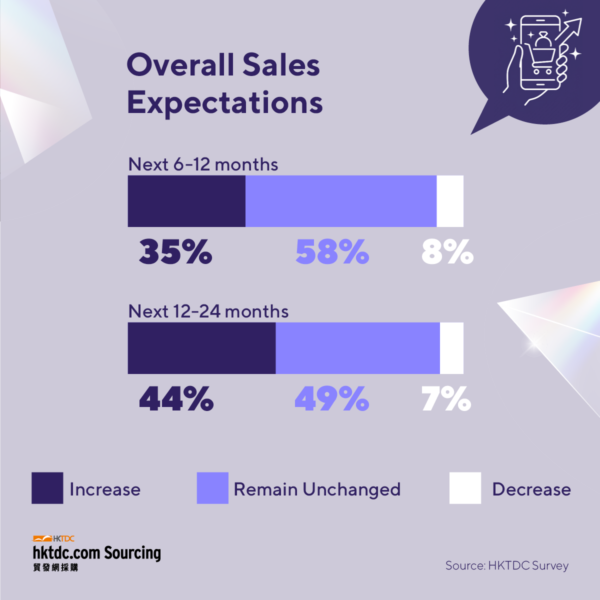

Moderate optimism over the next one to two years was observed of the 1,507 traders surveyed, among which 35% anticipated sales growth over the next 6‑12 months, while 58% believed their sales level would remain unchanged. Over the next one to two years, meanwhile, 44% of respondents expected an uptick in sales, while 49% anticipated their current level would be maintained.

In general, while traders are cautious about their near‑term prospects, they appear confident of gradual expansion over the medium term.

Opportunities and Challenges Co-Exist for the Global Jewellery Industry

A number of macroeconomic uncertainties look set to adversely impact 2026 jewellery sales, with more than half of all respondents seeing fluctuations in the global economy as a primary business concern. Among the other challenges highlighted were exchange‑rate volatility (37%) and inflationary pressures (34%), both of which were seen as likely to complicate business planning and implementation.

Amid these challenges, however, many traders have identified distinct opportunities. Deemed to have the highest potential is e‑commerce, which was cited by 41% of respondents. This was followed by rising demand in many of the emerging markets (35%), while about a third of all respondents had faith in recovering consumer purchasing power.

What Jewellery Product Categories Are Expected to Grow?

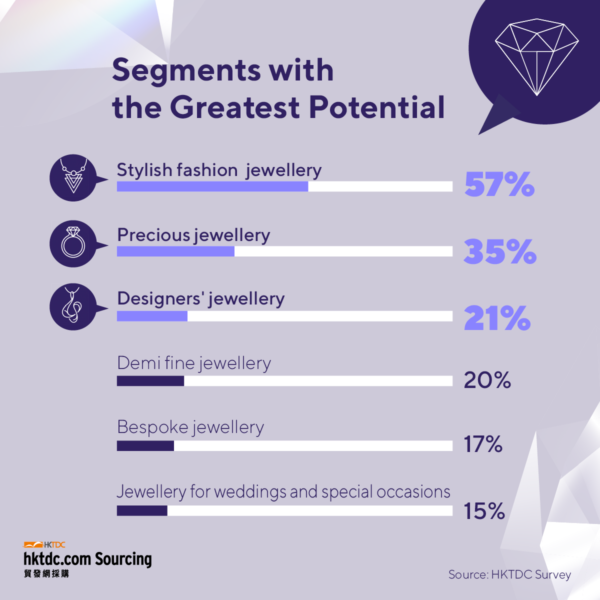

Stylish Fashion Jewellery Lead the Game

As with the past two years, stylish fashion jewellery and precious jewellery are the two segments seen as having the greatest growth potential (57% and 35%, respectively). Demand is strong for affordable, stylish items suitable for daily wear, which offer opportunities for self‑expression and targeted consumer appeal.

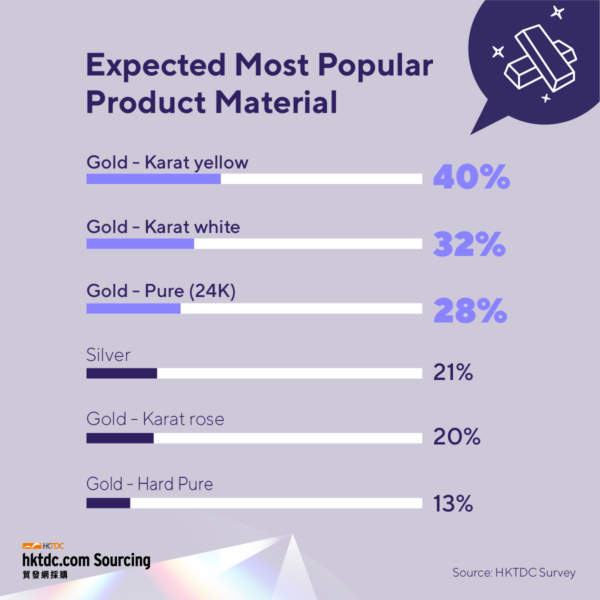

Gold Remains Most Popular Product Material

In terms of the most in‑demand precious metals, gold remains the most sought‑after, with karat yellow gold, karat white gold and 24K gold heading the category. Despite ongoing price volatility, demand for gold remains substantial, largely because of its high retention of value and familiarity as a safe‑haven asset. In line with this, the survey findings suggest higher prices have not diminished the appeal of gold and may, actually, have enhanced its structural investment values.

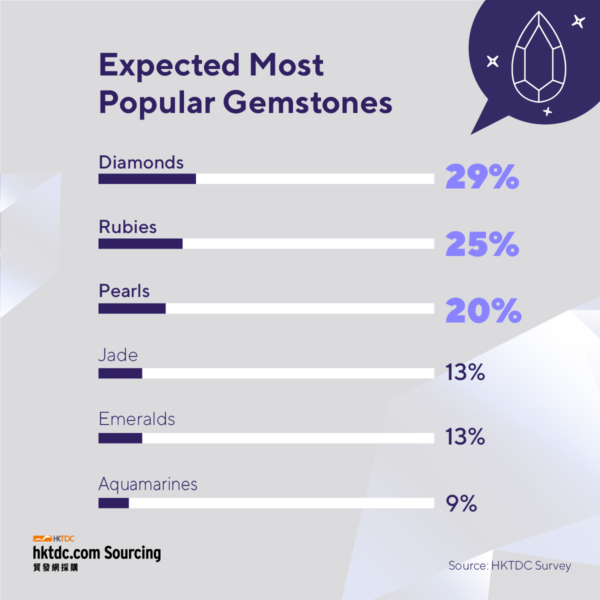

Favoured Gemstones Revealed

In the case of gemstones, preferences are less straightforward and more fluid. While diamonds remain the most favoured gemstones at 29%, rubies (25%) and pearls (20%) are not far behind. The relatively close spread across the three most popular gemstones can be taken as a sign of evolving consumer preferences, partly on account of the natural diamond market being under pressure from the rise of lab‑grown alternatives.

How Will the Jewellery Industry Transform in the Near Future?

Emerging Markets Take the Spotlight

When asked about the opportunities arising within the jewellery industry, it was anticipated that rebound in confidence would be fuelled by increased demand from a number of emerging markets. Specifically, South Korea (73.2%) and ASEAN (71.8%) were picked by over 70% of survey respondents as the most promising jewellery markets over the next two years. This was closely followed by the Chinese Mainland (68.5%), Taiwan (65.3%) and Australia (64.1%), all of which are key destinations for jewellery traders to explore.

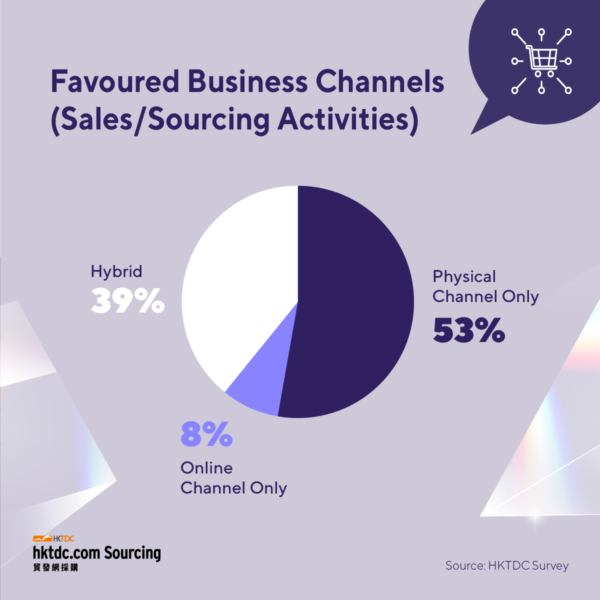

The Omnichannel Pivot

Within the jewellery sector, physical stores continue to be the primary channels in terms of both selling and sourcing, with 53% of respondents favouring such purchase routes. This is, perhaps, not surprising given that product aesthetics, craftsmanship and fit play decisive roles in jewellery purchases.

Despite this, there are signs that the omnichannel option is gaining traction, with 39% of respondents indicating they now favour a more hybrid approach amid global digitalization.

Summary

Rising e‑commerce opportunities and increased demand from emerging markets largely fuel the restoration of confidence among global jewellery traders. Respondents were moderately optimistic about the industry outlook in the next one to two years despite macroeconomic challenges.

As to the current state of the market, respondents saw stylish fashion jewellery and precious jewellery as the most in‑demand product segments, with gold‑karat yellow the preferred choice of metal. It was also noted that, while diamonds remain the most popular gemstone, rubies and pearls are finding increased favour.

Explore Full Survey Findings

Access detailed insights, including respondent profiles, via:

As identified from the survey findings, an omnichannel or hybrid approach is becoming vital to modern jewellery businesses. Whether you are a jewellery buyer or supplier, you will discover matching connections on our e-Marketplace and gain rewarding business benefits.

Access the world of facilitated jewellery trade 24/7 by clicking the following banner: